What is a Consumer Proposal?

A Consumer Proposal is a legally binding agreement arranged between you and your creditors, allowing you to settle your debts by paying a portion of what you owe or extending the time you have to pay off the debt. It’s an alternative to bankruptcy that can help you avoid many of the negative consequences associated with insolvency.

Benefits of a Consumer Proposal

Avoid Bankruptcy: A Consumer Proposal is an alternative to declaring bankruptcy, allowing you to manage your debt without the severe impact on your credit.

Debt Reduction: You may be able to settle your debts for less than what you owe.

Asset Protection: Unlike bankruptcy, a Consumer Proposal often allows you to keep your assets.

Legal Protection: Once your proposal is filed, creditors are legally barred from taking any further collection action.

Fixed Payments: Consolidate your debts into a single, affordable monthly payment.

Our Process

Free Initial Consultation: We start with a free consultation to assess your financial situation and determine if a Consumer Proposal is the right solution for you.

Personalized Proposal Development: Our team will work with you to develop a customized proposal that takes into account your financial capacity and the expectations of your creditors.

Negotiation with Creditors: We will negotiate on your behalf with your creditors to reach an agreement that benefits both parties.

Filing the Proposal: Once an agreement is reached, we will file the proposal with the Office of the Superintendent of Bankruptcy (OSB).

Approval and Implementation: After the creditors approve the proposal, you will make regular payments as agreed, and we will distribute these payments to your creditors.

Support and Guidance: Throughout the process, our team will provide ongoing support and guidance to ensure you stay on track with your payments and financial goals.

Why Choose Maple Leaf Associates?

Experienced Consultants: Our team includes professionals with FCI designations, Credit Specialists, and Master’s degrees in Accounting & Finance.

Personalized Service: We offer a personalized approach, tailoring each Consumer Proposal to fit your unique financial situation.

Proven Track Record: With 14 years of experience in Credit Management, our Lead Consultant is a member of the National Association of Credit Managers in Canada and the United States.

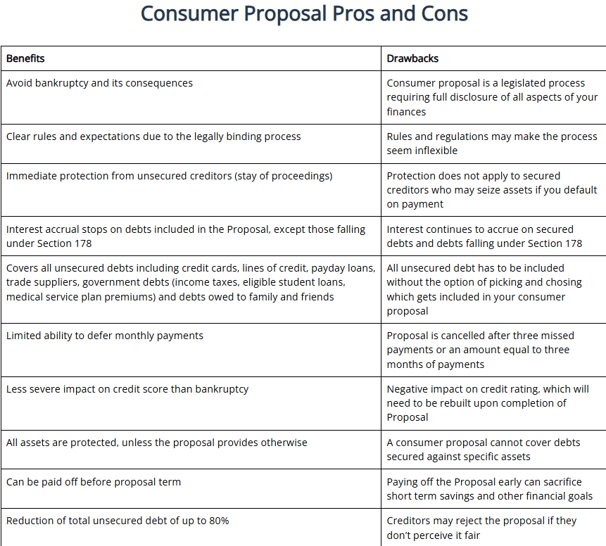

Consumer Proposal: Pros and Cons

A consumer proposal can be a helpful alternative to bankruptcy for those struggling with debt, but it’s essential to weigh both the benefits and drawbacks before deciding if it’s right for you. Here's a breakdown of the key pros and cons:

Benefits of a Consumer Proposal

✅ Avoid Bankruptcy and Its Consequences

A consumer proposal allows you to address your debt without the severe financial and personal impacts of bankruptcy.

✅ Clear Rules and Legally Binding

As a regulated process, a consumer proposal provides clear terms and expectations, offering a structured path to debt relief.

✅ Protection from Unsecured Creditors

Once filed, a consumer proposal immediately halts collection actions from unsecured creditors, providing relief from ongoing harassment.

✅ Interest on Debts Stops

Interest stops accruing on unsecured debts included in the proposal, reducing the overall amount you owe.

✅ Covers All Unsecured Debts

Consumer proposals cover a wide range of unsecured debts, including credit cards, lines of credit, payday loans, and even certain government debts.

✅ Credit Impact is Less Severe Than Bankruptcy

While there is a negative effect on your credit, it’s generally less severe and shorter than the impact of filing for bankruptcy.

✅ Asset Protection

Unlike bankruptcy, a consumer proposal allows you to retain ownership of your assets.

✅ Option to Pay Off Early

You have the flexibility to pay off the proposal sooner than planned, which can accelerate your journey to financial freedom.

✅ Debt Reduction Potential

With creditor approval, you may achieve a debt reduction of up to 80% on your unsecured obligations.

Drawbacks of a Consumer Proposal

⚠️ Full Financial Disclosure Required

The process mandates complete transparency regarding your finances, which some may find intrusive.

⚠️ Strict Rules and Regulations

Consumer proposals follow specific guidelines, which can sometimes feel rigid.

⚠️ Protection Excludes Secured Creditors

While unsecured debts are covered, secured creditors may still repossess assets if payments are missed.

⚠️ Interest Continues on Secured Debts

Interest on secured debts and specific debts under Section 178 will continue to accrue.

⚠️ Inclusion of All Unsecured Debts

You cannot selectively choose which unsecured debts are included—all must be part of the proposal.

⚠️ Limited Payment Deferrals

If you miss three payments (or an equivalent amount), the proposal may be cancelled, adding to financial pressure.

⚠️ Credit Impact

A consumer proposal negatively affects your credit score, requiring a focused effort to rebuild it afterward.

⚠️ Secured Assets Excluded

Debts secured against specific assets are not covered under the consumer proposal, meaning they’re still at risk.

⚠️ Early Payment May Affect Savings Goals

While paying off a proposal early is allowed, it may impact your ability to save or meet other financial objectives.

⚠️ Creditor Approval Required

If creditors view the proposal as unfair, they may reject it, prolonging your financial difficulties.

Consumer Proposal FAQs

1. What is a Consumer Proposal?

A consumer proposal is a legally binding agreement between you and your creditors to repay a portion of your debt over a specified period, typically up to five years. It is an alternative to bankruptcy and can help you reduce your total debt and make manageable payments.

2. Who is Eligible for a Consumer Proposal?

To be eligible for a consumer proposal, you must:

Owe between $1,000 and $250,000 (excluding the mortgage on your principal residence)

Be unable to pay your debts as they come due

Have a stable income to make the proposed payments

3. What Types of Debts Can Be Included in a Consumer Proposal?

Consumer proposals can help with unsecured debts, including:

Credit card debt

Tax debts

Student loans (if you have been out of school for at least seven years)

Bank loans

Payday loans

Lines of credit

Secured debts, such as mortgages and car loans, cannot be included in a consumer proposal.

4. How Does a Consumer Proposal Affect My Credit Rating?

Filing a consumer proposal will impact your credit rating. It will be noted on your credit report as an R7 rating, indicating that you have entered into a debt repayment plan. This rating will remain on your credit report for three years after you have completed the proposal.

5. Can Creditors Reject My Consumer Proposal?

Yes, creditors have the right to accept or reject your consumer proposal. If more than 50% of your creditors (by dollar value of the debt) vote to accept the proposal, it will be binding on all unsecured creditors. If the proposal is rejected, you may consider other debt relief options, such as bankruptcy.

6. Will Creditors Stop Harassing Me Once I File a Consumer Proposal?

Yes, once your consumer proposal is filed, all collection actions and legal proceedings against you must stop. Your creditors can no longer contact you directly; all communications will go through your Licensed Insolvency Trustee.

7. How Long Does It Take to Complete a Consumer Proposal?

The duration of a consumer proposal can vary but typically lasts up to five years. The exact length will depend on the terms negotiated with your creditors.

8. What Happens If I Miss a Payment?

If you miss three payments or fail to meet the terms of your consumer proposal, it will be deemed annulled, and your creditors can resume collection actions against you. It's crucial to communicate with your Licensed Insolvency Trustee if you encounter difficulties in making payments to explore possible solutions.

9. Can I Pay Off My Consumer Proposal Early?

Yes, you can pay off your consumer proposal early without any penalties. Doing so will help you rebuild your credit rating sooner and complete the process faster.

10. What Are the Advantages of a Consumer Proposal Over Bankruptcy?

A consumer proposal offers several advantages over bankruptcy, including:

Allowing you to retain your assets

Providing a structured repayment plan

Having less impact on your credit rating

Allowing you to avoid the stigma associated with bankruptcy

11. Do I Need a Licensed Insolvency Trustee to File a Consumer Proposal?

Yes, only a Licensed Insolvency Trustee (LIT) can administer a consumer proposal. They will work with you to develop the proposal, present it to your creditors, and manage the process.

12. How Can Maple Leaf Associates Help Me With a Consumer Proposal?

Maple Leaf Associates offers professional and personalized financial advice to help you navigate the consumer proposal process. Our experienced consultants will assess your financial situation, guide you through the proposal, and support you in achieving financial stability. Contact us today to learn more about how we can help you.

File a Debt Consumer Proposal with Maple Leaf Associates

Don’t wait for your debts, penalties, and interest charges to increase. For many, the first step toward a debt-free life involves filing a consumer proposal. With fewer, less expensive payments, consumer proposals are a less stressful way to face your debts head-on.

Maple Leaf Associates is a licensed insolvency trustee (LIT) providing specialist debt relief options to help you manage your financial troubles. We offer a range of debt relief services including debt consolidation and debt settlement.

Get in touch

For more information and personalized advice on Consumer Proposals, contact Maple Leaf Associates today. Our experienced consultants are here to help you navigate your financial challenges and find the best solution for your situation.

Phone

289-207-7449 / 437-603-6954

admin@mapleleafassociates.ca

Maple Leaf Associates

Solutions for individuals and companies in Ontario, Canada.

289-207-7449 437-603-6954

© 2025. All rights reserved.