Navigating Financial Challenges in Ontario: Understanding Consumer Proposals and Personal Bankruptcy

11/9/20249 min read

Introduction to Financial Challenges in Ontario

Ontario, one of Canada’s most populous provinces, is experiencing a complex financial landscape characterized by a multitude of challenges faced by its residents. With a diverse economy, the province is home to both thriving industries and struggling sectors, which contributes to fluctuating employment rates and financial uncertainty. Rising levels of personal debt have become increasingly prevalent, influencing the financial well-being of individuals and families alike.

The phenomenon of rising debt can be attributed to several factors, including increased living costs, particularly in urban centers such as Toronto and Ottawa, where housing prices and rents have soared. This has led many residents to rely on credit to maintain their lifestyles, resulting in unsustainable debt burdens. Furthermore, economic instability has been exacerbated by external factors such as global trade tensions, fluctuating interest rates, and the lasting effects of the COVID-19 pandemic. The pandemic not only altered employment landscapes, causing layoffs and reduced working hours, but it also heightened financial precarity for many households.

The COVID-19 pandemic has left an indelible mark on the financial health of Ontarians; many found themselves grappling with job insecurity and unexpected expenses related to health care and remote working arrangements. As a result, thousands of individuals turned to credit cards and loans to navigate through the crisis, further intensifying their debts. These challenges have underscored the critical need for effective debt management strategies and an informed understanding of the available options for financial relief.

Addressing these challenges requires comprehensive knowledge of the potential solutions, including consumer proposals and personal bankruptcy, which will be explored further in this blog post. By equipping oneself with the right information, residents can better navigate their financial difficulties and make informed decisions to regain control over their economic futures.

What is a Consumer Proposal?

A consumer proposal is a formal, legally binding agreement between a debtor and their creditors under Canadian law, specifically designed to help individuals manage their financial challenges. This financial arrangement serves as an alternative to declaring personal bankruptcy, enabling debtors to repay a portion of their debts while providing them with protection from their creditors. It is often a more manageable solution for individuals who find themselves overwhelmed by financial obligations but wish to avoid the long-term repercussions associated with bankruptcy.

When a consumer proposal is filed, it must be prepared by a licensed insolvency trustee (LIT), who will assess the debtor's financial situation and negotiate the terms with the creditors. The proposal typically outlines a clear payment plan that specifies how much the debtor can afford to pay each month and over what duration, usually ranging from three to five years. The terms of the consumer proposal must be approved by a majority of the creditors, who may agree to accept a reduced total amount owed, thus allowing the debtor to avoid the total loss associated with bankruptcy.

In most cases, the proposed payment plan is a percentage of the total debt, which is significantly less than what the debtor would need to pay without the proposal. This alleviates some of the pressure on the individual while providing creditors with a better chance of recovering some of their losses. Moreover, during the proposal period, creditors are not allowed to initiate collection actions or garnishments, giving debtors much-needed peace of mind during this challenging time.

In summary, a consumer proposal is a viable option for individuals struggling with debt, offering a structured way to settle financial obligations while avoiding the severe impacts of personal bankruptcy.

What is Personal Bankruptcy?

Personal bankruptcy is a legal process designed to provide individuals who are unable to repay their debts with a fresh financial start. It allows debtors to declare their inability to meet financial obligations and seek relief from some or all of their debts. This legal status is typically adjudicated in a bankruptcy court, where the debtor can formalize their financial situation and obtain protection from creditors. In Ontario, the process often begins with an assessment of the individual's financial position, debts, and ability to repay them.

When an individual files for personal bankruptcy, they must work with a licensed insolvency trustee (LIT) who will help guide them through the entire process. The LIT assists in preparing the necessary documentation, negotiating with creditors, and administering the bankruptcy estate. Upon declaration, an automatic stay is placed on creditor actions, meaning that creditors cannot pursue collection activities while the bankruptcy process is underway. This provides the debtor with breathing room to navigate their financial challenges.

It is essential to understand the legal implications of declaring personal bankruptcy. For the debtor, this may include the loss of certain assets and a negative impact on credit ratings, which can last for several years. Conversely, for creditors, personal bankruptcy limits their ability to collect on debts owed by the bankrupt individual, often leading to a portion of the debt being discharged or settled. This contrasts with other forms of bankruptcy, such as corporate bankruptcy, which typically involves businesses rather than individuals. Corporate bankruptcy addresses debts incurred by companies and may involve more complex legal proceedings.

Comparing Consumer Proposals and Personal Bankruptcy

Understanding the differences between consumer proposals and personal bankruptcy is essential for individuals facing financial challenges in Ontario. Both options serve to address unmanageable debts but differ significantly in various aspects, such as eligibility criteria, creditor payments, legal protections, timelines, and implications for credit scores.

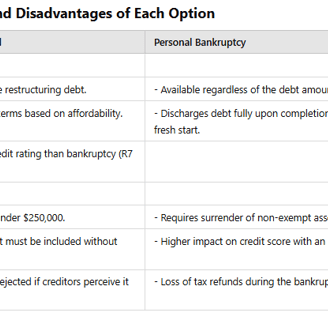

To begin with, eligibility criteria for consumer proposals are generally more lenient compared to personal bankruptcy. A consumer proposal can be filed by individuals with unsecured debts not exceeding $250,000 (excluding the mortgage on their primary residence). On the other hand, personal bankruptcy is available to anyone in Ontario who cannot meet their financial obligations, regardless of the debt amount. However, it is crucial to note that the bankruptcy process involves more stringent requirements and potentially more severe consequences.

When it comes to creditor payments, consumer proposals allow individuals to negotiate a repayment plan, often resulting in reduced payments over a set period, usually lasting up to five years. In contrast, personal bankruptcy may lead to a complete discharge of debts after a shorter period, though it may involve selling non-exempt assets to satisfy creditor claims. This distinction is vital for those considering how to manage their financial burdens while protecting their assets.

Legal protections also differ between these two options. A consumer proposal provides a stay of proceedings, preventing creditors from taking legal action or contacting the debtor during the proposal's term. In contrast, while personal bankruptcy offers similar protections, it may not provide the same level of benefits, particularly for individuals who may not own assets. Furthermore, the timeline for personal bankruptcy is typically shorter, with discharges occurring between nine months to two years, depending on the individual's circumstances.

From a credit score perspective, both consumer proposals and personal bankruptcy impact an individual's credit rating. A consumer proposal remains on the credit report for three years after completion, whereas a personal bankruptcy can last up to six or seven years, depending on the number of filings. Such differences can shape individuals' post-debt recovery and ability to secure future credit.

Benefits and Drawbacks of Consumer Proposals and Personal Bankruptcy

Navigating financial challenges in Ontario often involves difficult decisions between consumer proposals and personal bankruptcy. Both options have their respective advantages and drawbacks, which are crucial to consider when determining the best route to alleviate financial distress.

One of the primary benefits of a consumer proposal is that it allows individuals to preserve their assets while negotiating a manageable repayment plan with creditors. This option provides a structured approach to addressing debts, typically involving a reduced payment amount over a specified term, generally up to five years. Moreover, consumer proposals have a less severe impact on credit ratings compared to personal bankruptcy, which can last for up to seven years or more on one’s credit report. This makes it a more attractive choice for individuals keen on rebuilding their creditworthiness quickly.

On the other hand, personal bankruptcy can provide immediate relief from overwhelming debt. It eliminates the obligation to pay most unsecured debts, offering a fresh start for individuals facing insurmountable financial hardship. For some, this may be the most feasible option to regain financial stability. However, it is essential to recognize the long-term implications; a bankruptcy filing may significantly damage one’s credit profile and can carry a societal stigma that may affect personal and professional relationships.

Another drawback of personal bankruptcy is the potential requirement to surrender certain assets, a stark contrast to the preservation capability afforded by a consumer proposal. Ultimately, the impact on credit scores, the stigma associated with bankruptcy, and the loss of assets are critical issues to weigh against the benefits of immediate debt relief and the structured repayment found in a consumer proposal.

Steps to Take When Considering Your Options

When facing financial challenges in Ontario, it becomes essential for individuals to understand the steps necessary to navigate their options effectively. The first step involves seeking financial advice from a trusted source. Engaging with a financial advisor or counselor can provide invaluable insights into one’s fiscal situation and available alternatives. These professionals can assist in understanding the implications of both consumer proposals and personal bankruptcy, thus allowing individuals to make informed decisions based on their unique circumstances.

After obtaining initial financial guidance, the next critical step is consulting with a licensed insolvency trustee (LIT). LITs are certified professionals who specialize in managing insurmountable debts. They provide a comprehensive overview of the consumer proposal process, outlining how it can help achieve debt relief without resorting to bankruptcy. Additionally, LITs can clarify the potential impact of personal bankruptcy, ensuring that individuals fully grasp the long-term consequences of each option.

Furthermore, it is crucial to evaluate one’s personal financial situation thoroughly. This involves conducting a thorough analysis of income, expenditures, debts, and assets. A detailed assessment allows individuals to determine whether negotiating a consumer proposal may be more viable than declaring personal bankruptcy, or vice versa. Keeping accurate records of these financial details is essential when preparing for discussions with the insolvency trustee and creditors.

Lastly, preparing for meetings with creditors is a vital step in the process. Individuals must be equipped with necessary documentation, including income statements, tax returns, and detailed lists of liabilities. This preparation not only enhances the effectiveness of negotiations but also demonstrates a commitment to resolving the financial situation responsibly. By following these practical steps, Ontario residents can strategically approach their financial challenges while considering whether to pursue a consumer proposal or personal bankruptcy.

Conclusion and Next Steps

Throughout this blog post, we explored critical financial challenges faced by individuals in Ontario, specifically focusing on the options of consumer proposals and personal bankruptcy. Both solutions serve as viable pathways for protecting oneself from overwhelming debt, but they come with distinct implications that must be carefully considered. Understanding the nuances of these processes is essential in navigating financial hardships effectively.

Consumer proposals offer a structured alternative to bankruptcy, allowing borrowers to renegotiate their debts and make manageable payments over time. This option not only provides a potential reduction in the total debt owed but also helps individuals avoid the severe repercussions of bankruptcy, such as the loss of assets and damage to credit ratings. On the other hand, personal bankruptcy may be necessary for someone unable to fulfill their financial obligations. While it offers a clean slate, it carries significant long-term consequences that could impact future financial endeavors.

As we have discussed, the right choice between these options will vary depending on individual circumstances, such as income level, amount of debt, and assets possessed. Taking the time to evaluate one's own financial situation is a critical first step in making a well-informed decision. Seeking assistance from professionals, such as credit counselors or licensed insolvency trustees, is strongly encouraged to navigate these complex options further.

In conclusion, confronting financial difficulties can be overwhelming, but it is essential to understand the available tools to regain control. By proactively seeking guidance and exploring both consumer proposals and personal bankruptcy, individuals can make informed choices that best suit their financial well-being. Taking these steps can lead not only to financial recovery but also to renewed opportunities for a stable economic future.

Impact on Credit Score and Financial Future

Both consumer proposals and bankruptcy impact your credit, but to different extents and durations.

Consumer Proposal: Filing a consumer proposal results in an R7 credit rating, which reflects a negotiated settlement. This rating stays on your credit report for three years after you complete the proposal, which could last up to five years. While an R7 rating is still negative, it is less severe than a bankruptcy rating, making it easier to rebuild credit after completion.

Personal Bankruptcy: Bankruptcy has a more significant impact on your credit score. A first-time bankruptcy filing results in an R9 rating, the lowest possible, which remains on your credit report for six years after discharge. A second bankruptcy stays on your report for 14 years, which can hinder future borrowing opportunities and access to credit.

Legal Protection from Creditors

Both options provide legal protection, called a “stay of proceedings,” which stops most creditor actions against you.

Consumer Proposal: Once a consumer proposal is filed, it provides immediate protection from unsecured creditors, stopping collection calls, wage garnishments, and other legal actions. However, this protection does not extend to secured creditors, such as mortgage lenders, who can still seize assets if payments are missed.

Personal Bankruptcy: Bankruptcy also provides a stay of proceedings, offering similar protection against unsecured creditors. However, like in a consumer proposal, secured creditors retain their rights over collateralized assets and may enforce repossession if payments are not kept up.

Advantages and Disadvantages of Each Option

How to Decide: Consumer Proposal or Bankruptcy?

Deciding between a consumer proposal and bankruptcy depends on your specific financial situation, debt level, and long-term goals. Consider the following:

Asset Retention: If keeping your assets is a priority, a consumer proposal may be a better option, as it allows you to keep your property.

Debt Level: If your debt level exceeds $250,000, bankruptcy may be the only available option.

Flexibility Needs: If you need flexible payments, a consumer proposal offers a structured payment plan that can be adjusted to suit your financial circumstances.

Impact on Future Finances: If you want to minimize the long-term impact on your credit score, a consumer proposal will generally have a lesser effect than bankruptcy.

Get in touch

Share with visitors how they can contact you and encourage them to ask any questions they may have.

Maple Leaf Associates

Solutions for individuals and companies in Ontario, Canada.

289-207-7449 437-603-6954

© 2025. All rights reserved.